Do I Need A Financial Adviser?

Introduction

Many people never seek financial guidance or financial advice, often because they are unsure where to start, concerned about costs, or uncertain whether they need help at all.

Others may have accumulated pensions, investments and savings over many years but are unsure how these fit together, whether they are on track for retirement, or what options may be available to them.

The reality is that there is no single "correct" approach. Some people are comfortable researching and managing their finances themselves. Others benefit from reassurance, financial guidance and modelling services, such as those provided by Clear Thinking Finance UK, while some situations may warrant the protection and recommendations offered through regulated financial advice.

Understanding the differences between these options can help you make more informed decisions about the support you require, the costs involved and the value each approach may provide.

This guide explores some of the key areas where individuals commonly seek assistance, including retirement planning, investing, tax planning, inheritance considerations and product selection. It also explains what financial advisers do, where financial guidance can help, and how to identify the most appropriate support for your circumstances.

Key Takeaways

DIY can be appropriate for many people.

Financial guidance can help improve understanding and test scenarios.

Regulated advice provides personal recommendations and regulatory protections.

Charges, investment performance and planning value should all be considered.

The right choice depends on your objectives, confidence and circumstances.

Contents

1.What Does a Financial Adviser Actually Do?

Many people associate financial advice primarily with investment performance. While investments often form part of the advice process, the role of a financial adviser is usually much broader than simply selecting funds or attempting to achieve higher returns.

At its core, financial advice is about helping individuals make informed decisions and develop a plan to achieve their financial objectives. This may involve understanding what those objectives are, assessing current circumstances, identifying potential risks and opportunities, and recommending suitable courses of action.

Depending on a person's circumstances, financial advice may cover areas such as:

• Retirement planning and retirement timing

• Pension contribution strategies

• Pension consolidation considerations

• Investment planning

• Tax planning

• Inheritance tax and estate planning

• Protection planning

• Cashflow modelling and affordability analysis

• Retirement income and withdrawal strategies

• Structuring assets efficiently

• Gifting and intergenerational planning

• Behavioural support during periods of market uncertainty

A financial adviser will normally gather information about your circumstances, objectives, income, assets, liabilities, attitude to risk and capacity for loss before making any personal recommendations.

The implementation of recommendations may involve selecting suitable products, providers, investment solutions or discretionary investment managers, together with ongoing reviews to ensure arrangements remain aligned with your objectives.

While investment performance is undoubtedly important, many advisers would argue that their greatest value often comes from helping clients make better decisions, avoid costly mistakes and maintain a long-term plan through changing personal and economic circumstances.

2.Financial Planning vs Wealth Management

The terms financial planning and wealth management are often used interchangeably, but they can represent different aspects of helping individuals achieve their financial objectives.

Financial planning focuses on understanding what you want to achieve and creating a strategy to help get there. The starting point is typically your goals, lifestyle aspirations and future plans rather than specific products or investments.

Examples of financial planning discussions may include:

• Can I afford to retire when I want to?

• How much can I spend in retirement?

• Should I increase pension contributions?

• Can I help my children financially?

• What impact could care costs have on my finances?

• How might inheritance tax affect my estate?

• Am I taking unnecessary financial risks?

The emphasis is on identifying objectives, modelling different scenarios and developing a plan to achieve them.

Wealth management often places greater emphasis on the management of investments and assets, although many firms provide both services. This may include investment selection, portfolio construction, discretionary fund management, ongoing investment reviews and ensuring assets remain aligned with a client's agreed risk profile and objectives.

In practice, there is often significant overlap between the two disciplines. Good wealth management should support a financial plan, while good financial planning should take account of how assets are invested and managed.

For many people, financial planning is where the most important questions are answered. Once objectives have been identified and a strategy developed, products, investments and wealth management solutions become tools that may help support those goals.

Understanding this distinction can be useful when deciding what type of support you require and where professional help may add the greatest value.

For example, you may feel comfortable planning your finances and defining your objectives yourself, but prefer assistance with investment selection and portfolio management. In these circumstances, a wealth management-focused proposition may be particularly attractive.

Conversely, your primary focus may be retirement planning, tax efficiency, inheritance considerations, product selection or understanding whether your long-term goals are achievable. In these cases, you may place greater value on a planner-led approach, where financial planning forms the core of the relationship and investment management is supported by an in-house investment team or external specialist provider.

Others may prefer a combination of both, working with an adviser who can provide comprehensive financial planning support while also discussing and overseeing investment decisions directly.

The most appropriate approach will depend on your objectives, the complexity of your circumstances and the areas where you feel professional support is likely to add the greatest value.

3.DIY, Financial Guidance or Financial Advice?

Once you have identified the areas where support may be beneficial, the next consideration is how you wish to obtain that support.

Broadly speaking, there are three approaches available whether used fully or in combination:

• Managing your finances yourself (DIY)

• Using a financial guidance service

• Seeking regulated financial advice

Each option has advantages and disadvantages, and the most appropriate choice will depend on your objectives, confidence, available time and the complexity of your circumstances.

Managing Your Finances Yourself

Many people successfully manage their own finances using online resources, books, calculators, investment platforms and educational content.

A DIY approach can provide complete control over decision-making, lower ongoing costs and the opportunity to build financial knowledge and confidence.

However, it also requires a willingness to research options, understand risks, keep up with changing legislation and regularly review plans as circumstances evolve.

Financial Guidance

Financial guidance sits between DIY decision-making and regulated financial advice.

The purpose of guidance is to help individuals better understand their options, improve financial knowledge and explore different scenarios without receiving personal recommendations.

Examples may include:

• Retirement affordability modelling

• Understanding pension options

• Exploring retirement timing

• Considering inheritance planning scenarios

• Understanding the implications of different decisions

• Identifying areas that may require further investigation

4.Investment Decisions

One of the most common reasons people seek financial guidance or regulated financial advice is assistance with investment decisions.

For some individuals, investing can appear relatively straightforward. A wide range of online platforms, educational resources and investment tools are available, making it possible to research investments and construct portfolios independently.

For others, questions may arise such as:

• How much investment risk should I take?

• Am I invested appropriately for my objectives?

• Should I be actively managing investments or using a simpler approach?

• How diversified is my portfolio?

• How should investments change as I approach retirement?

• Am I paying reasonable charges?

DIY

Many investors successfully manage their own investments by researching asset classes, understanding diversification principles and selecting investments through direct-to-consumer platforms.

There are also a growing number of solutions designed for investors who prefer a simpler approach. These include ready-made portfolios that automatically invest across a range of underlying funds based on a chosen level of risk, together with multi-asset funds that provide diversified exposure through a single investment.

Such solutions can reduce the complexity of investment selection and ongoing management while still providing exposure to a broad range of asset classes.

A DIY approach can provide greater control and potentially lower costs, but it also requires time, ongoing learning and a willingness to review decisions as circumstances and objectives change over time.

Financial Guidance

Financial guidance can help investors better understand concepts such as risk, diversification, asset allocation, investment charges and the potential advantages and disadvantages of different approaches.

Guidance may also help individuals understand how investment decisions interact with wider financial objectives, such as retirement plans, future spending requirements or inheritance goals.

However, guidance does not provide personal recommendations regarding specific investments, products or providers.

Regulated Financial Advice

Regulated financial advice may be beneficial where investors require recommendations tailored to their circumstances.

This may include assessing attitude to risk and capacity for loss, recommending suitable investment solutions, selecting products and providers, and ensuring investment strategies remain aligned with wider financial planning objectives.

Some advisers manage investments directly, while others utilise model portfolios, discretionary fund managers (DFMs) or specialist investment teams as part of their investment proposition.

The most appropriate approach will depend on the complexity of your circumstances, your confidence in making investment decisions and the value you place on professional support.

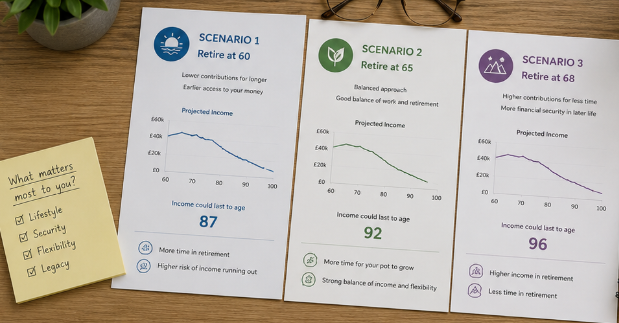

5.Retirement Planning and Sustainability

For many people, retirement planning is not about choosing investments or selecting products. It is about answering a much more fundamental question:

Will I have enough money to support the lifestyle I want throughout retirement?

This is one of the areas where financial planning, financial guidance and regulated advice can all play a role.

Common questions include:

• When can I afford to retire?

• How much can I spend each year?

• How long might my money last?

• Should I take tax-free cash?

• Is drawdown or an annuity more appropriate?

• Can I help children or grandchildren financially?

• What impact could care costs have?

• How much can I safely withdraw from my investments?

• Will I leave an inheritance?

Retirement planning is often more complex than simply comparing income and expenditure today. Circumstances can change significantly over time, with spending often varying throughout retirement as health, lifestyle and priorities evolve.

Many people also underestimate future expenditure by focusing primarily on essential household costs. A more comprehensive approach may consider lifestyle aspirations, travel plans, hobbies, family support, home improvements, gifting intentions and potential later-life care requirements.

One useful exercise is to consider retirement spending across three broad categories:

• Essential expenditure – costs that must be met regardless of circumstances

• Desirable expenditure – spending that improves quality of life but may be flexible

• Aspirational expenditure – lifestyle goals, major purchases and discretionary spending

This can help provide a clearer understanding of what retirement may realistically cost and the level of flexibility available if circumstances change.

DIY

Many individuals undertake retirement planning independently using calculators, online tools and personal budgeting exercises.

This can be entirely appropriate where circumstances are relatively straightforward and there is confidence in making assumptions regarding future expenditure, investment returns and inflation.

However, retirement planning often requires assumptions to be made over periods of twenty, thirty or even forty years, making outcomes particularly sensitive to small changes in assumptions.

Financial Guidance

Financial guidance can help individuals explore different scenarios and better understand how decisions may affect future outcomes without receiving personal recommendations.

This is an area where many people benefit from support before considering whether regulated financial advice is required. Rather than focusing on product selection or investment recommendations, the emphasis is on understanding objectives, assessing affordability and exploring the implications of different choices.

Examples may include:

• Comparing different retirement ages

• Assessing the impact of increased pension contributions

• Understanding retirement affordability

• Exploring gifting scenarios

• Considering the potential impact of care costs

• Understanding how different retirement income strategies may affect sustainability

• Reviewing how changes to expenditure could affect future outcomes

• Exploring different inheritance planning scenarios

Financial guidance can also utilise specialist cashflow modelling software to help build a picture of how pensions, savings, investments, expenditure and future goals may interact over time. At Clear Thinking Finance UK, we use the same cashflow modelling tools used by many financial advisers to help illustrate the potential impact of different decisions before they are made.

Scenarios can then be stress tested using different assumptions, such as lower investment returns, higher inflation, increased expenditure or changes in life expectancy, helping individuals understand how robust their plans may be under different circumstances.

At Clear Thinking Finance UK, helping individuals identify objectives, estimate future expenditure requirements and explore different scenarios through cashflow modelling forms a core part of the service offered.

This can provide significant value for those seeking greater certainty around retirement affordability and future planning, while avoiding the need for personal recommendations where they are not required and potentially reducing the overall cost of obtaining financial support.

Regulated Financial Advice

The key distinction between financial guidance and regulated financial advice is not necessarily the complexity of the situation, but the ability to provide personal recommendations and implement solutions.

Where guidance focuses on helping individuals understand their options, explore scenarios and assess potential outcomes, regulated financial advice can recommend specific courses of action, products, providers and investment solutions based on an individual's circumstances and objectives.

Examples may include recommendations regarding:

• Pension and retirement income strategies

• Investment portfolios

• Product and provider selection

• Tax-planning arrangements

• Estate planning solutions

• Protection requirements

• Implementation of financial strategies

Regulated advice also provides access to additional consumer protections and a formal suitability process, with advisers responsible for ensuring recommendations are appropriate for the client's circumstances, objectives, attitude to risk and capacity for loss.

It is important to understand that these protections do not guarantee positive investment performance or protect against normal market movements. Investments can rise and fall in value, and outcomes may differ from expectations. The focus of the suitability process is on ensuring that the recommendations made were appropriate based on the information available at the time, that the risks were clearly explained and that the rationale for the recommendations was documented.

For some individuals, financial guidance and modelling may provide all the clarity required to proceed independently. For others, it can help identify areas where a personal recommendation would be beneficial and provide a clearer understanding of what they wish to achieve before engaging an adviser.

6.Tax Planning and Inheritance Tax Considerations

Tax planning and inheritance tax (IHT) considerations are often areas where individuals seek assistance, particularly as wealth accumulates and retirement approaches.

While many people focus on investment performance and pension values, the amount ultimately retained by you or passed to future generations can also be significantly influenced by tax planning decisions.

Ensuring available tax allowances are being utilised effectively is often one of the simplest ways to improve tax efficiency. For couples, it can also be important to consider how assets and allowances are used across both individuals rather than viewing each person in isolation.

Common questions include:

• Am I using available tax allowances efficiently?

• Should I prioritise pensions, ISAs or other investments?

• Can I make gifts to family members?

• How much inheritance tax could be payable on my estate?

• What impact could future legislation have?

• Should I spend, gift or retain assets?

• How should assets be held between spouses or partners?

• What happens to my pensions and investments on death?

Tax planning is not always about reducing tax though. In many cases it is about understanding the implications of decisions before they are made and ensuring arrangements remain aligned with wider financial objectives.

DIY

Many individuals successfully undertake basic tax planning themselves by making use of available allowances and understanding the tax treatment of common financial products, gifting and their IHT position for their estate.

However, as circumstances become more complex, it can become increasingly difficult to assess how different assets interact and what the long-term consequences of certain decisions may be.

Financial Guidance

Financial guidance can help individuals better understand the tax treatment of pensions, ISAs, investments and estate planning arrangements, together with the potential implications of gifting, spending and wealth transfer decisions.

Examples may include:

• Exploring inheritance tax scenarios - current exposure and potential position

• Understanding gifting rules and allowances

• Reviewing how assets are structured

• Considering the impact of pension death benefits and future legislative changes.

• Understanding how different products are taxed

• Identifying areas that may warrant further investigation

This can help individuals make more informed decisions and identify where specialist advice may be beneficial.

Regulated Financial Advice

Regulated financial advice may be valuable where an individual requires personal recommendations regarding tax-planning strategies, product selection, estate planning arrangements or the implementation of financial solutions.

While financial guidance can help individuals understand their options and the potential implications of different decisions, advisers can recommend specific courses of action based on an individual's circumstances and objectives.

Examples may include recommendations regarding:

• Gifting strategies

• The use of trusts

• Product and provider selection

• Estate planning arrangements

• Business Relief investments

• Pension death benefit planning

• Asset structuring

• Tax-efficient investment solutions

Advisers can also assist with the implementation of recommendations and provide ongoing reviews as circumstances, legislation and objectives evolve over time.

It is also worth recognising that tax legislation changes regularly. Strategies that are appropriate today may require review in the future as personal circumstances, legislation and objectives evolve.

7.Understanding Charges

Charges are often one of the most discussed aspects of financial planning and investment management. Whilst costs are important, they should generally be considered alongside the value being provided and the objectives being achieved.

Depending on the route chosen, there may be several layers of charges to consider.

DIY

For those managing their own finances, costs will often be limited to platform and investment charges.

This can be an attractive option for individuals who are confident making decisions independently and willing to undertake their own research, monitoring and administration.

However, lower charges do not automatically lead to better outcomes. The value of professional support, planning, governance and behavioural coaching should also be considered where relevant.

Financial Guidance

Financial guidance will typically involve a clearly defined fee for the service being provided, often agreed in advance and independent of any products, investments or assets being considered.

As financial guidance does not involve personal recommendations or the implementation of products, there are generally no ongoing adviser charges associated with the service unless further guidance sessions are requested in the future.

Financial guidance can also help individuals understand the various charges that may apply across existing arrangements and how they interact with one another.

Examples may include:

• Identifying the different layers of charges

• Comparing costs across different solutions

• Understanding the impact of charges over time

• Assessing whether services being paid for are being utilised

• Reviewing whether existing arrangements remain appropriate

• Understanding the potential costs of regulated financial advice and discretionary investment management

For some individuals, financial guidance may provide sufficient clarity to proceed independently. For others, it may help identify areas where regulated financial advice would be beneficial whilst providing a clearer understanding of the likely costs involved.

This can help individuals make more informed decisions and better understand the value they are receiving relative to the charges being incurred.

Regulated Financial Advice

Financial advisers typically charge either a percentage of assets under management, a fixed fee, or a combination of the two.

Percentage-based ongoing adviser charges commonly range from around 0.5% to 1.0% per annum (plus VAT where applicable), although this can vary significantly depending on the level of service being provided and the complexity of the client's circumstances.

Some clients question why they may pay the same percentage-based adviser charge as another client with significantly lower levels of wealth.

Advisory firms will often argue that the complexity of circumstances, professional responsibility, regulatory obligations, ongoing monitoring requirements and potential liability associated with providing advice do not necessarily increase or decrease in direct proportion to the size of a portfolio. In addition, larger portfolios may involve more complex tax planning, estate planning and retirement income considerations.

However, it is also reasonable for clients to consider whether the charges being incurred remain proportionate to the level of service and value being received. If you feel this may not be the case, it is entirely appropriate to discuss this with your adviser. Some firms offer tiered charging structures, discounted rates for larger portfolios or bespoke fee arrangements where circumstances warrant this.

Some advisers may instead offer fixed-fee arrangements, although these can be less common and may not always be suitable for every client.

It is important to understand that adviser charges are often only one component of the overall cost. Depending on the solution being recommended, there may also be platform charges, investment fund charges and, where applicable, discretionary investment management charges.

As a result, the total cost of ownership can sometimes be higher than initially expected if all layers of charges are not considered together.

When assessing charges, useful questions may include:

• What services am I receiving?

• How often will reviews take place?

• What support is available between reviews?

• What ongoing work is being carried out on my behalf?

• How are investments being monitored?

• Are there additional DFM or platform charges?

• What is the total annual cost once all charges are combined?

Ultimately, charges should not be viewed in isolation. A lower-cost solution that fails to meet your objectives may be poor value, whilst a higher-cost solution that delivers meaningful planning, support and confidence may represent excellent value.

The key consideration is whether the service, expertise and support being provided justify the costs being incurred.

8.The Protection Provided by Regulated Advice

One of the key distinctions between financial guidance and regulated financial advice is the level of consumer protection that accompanies a personal recommendation.

Before providing advice, advisers are required to gather information regarding a client's circumstances, objectives, attitude to risk and capacity for loss. Recommendations must then be supported by a documented suitability assessment explaining why the adviser believes a particular course of action is appropriate.

This process is designed to help ensure recommendations are aligned with the client's needs and objectives and that the risks involved are clearly explained.

Regulated advice can provide protection in areas such as:

• The suitability of recommendations

• Disclosure of risks

• Adviser qualifications and regulatory standards

• Access to complaints procedures

• Access to the Financial Ombudsman Service where appropriate

• Financial Services Compensation Scheme (FSCS) protection where applicable

It is important to understand what these protections do and do not cover.

The protections associated with regulated advice do not guarantee positive investment performance, prevent losses arising from normal market movements or ensure that investments will achieve a particular outcome.

Investments can rise and fall in value and actual results may differ from expectations. The purpose of the suitability process is not to eliminate investment risk, but to ensure that any recommendations made were appropriate based on the information available at the time, that the risks were properly explained and that the rationale for the recommendation was clearly documented.

This distinction is important because many people incorrectly assume that poor investment performance automatically means advice was unsuitable. In reality, an investment may perform poorly due to market conditions whilst still having been an appropriate recommendation based on the client's objectives, risk tolerance and circumstances when the advice was given.

Regulated advice can therefore provide valuable protection around the process, suitability and implementation of financial decisions. However, it should still be assessed alongside the costs involved and the value being provided, particularly where an individual is comfortable making certain decisions independently.

For some people, the reassurance provided by a regulated recommendation and the associated consumer protections can be a significant benefit. For others, financial guidance may provide sufficient understanding and confidence without requiring personal recommendations.

9.How to Find a Financial Adviser

If, after considering your options, you decide that regulated financial advice may be beneficial, the next step is finding an adviser whose approach, services and charging structure align with your needs.

Many people begin their search through personal recommendations from family, friends or colleagues. Whilst recommendations can be valuable, it is important to remember that an adviser who is suitable for one individual may not necessarily be the best fit for another.

Useful resources when searching for an adviser include:

• Unbiased

• VouchedFor

• The Personal Finance Society (PFS)

• Chartered Institute for Securities & Investment (CISI)

• Professional connections and personal recommendations

When reviewing potential advisers, consider not only qualifications and reviews, but also how the firm operates and the services it provides.

Questions worth exploring may include:

• Are they Independent or Restricted?

• Do they specialise in particular planning areas or client groups? For example, retirement planning, inheritance tax planning, business owners, legal professionals, media professionals or sports professionals.

• What services do they provide?

• How are they paid?

• Do they use a Discretionary Fund Manager (DFM)?

• Do they operate a centralised investment proposition?

• What level of ongoing service is offered?

• How often are reviews carried out?

• What qualifications do the advisers hold?

Do You Need a Minimum Level of Wealth?

A common misconception is that financial advisers only work with wealthy individuals.

Whilst some advisory firms do specialise in higher-net-worth clients and may have minimum asset levels, this is not true of the profession as a whole. Firms will vary on any minimum asset levels, minimum fees or other criteria that help determine whether they are able to provide a service that is commercially viable for both the client and the firm.

In practice, the question is often less about how much wealth you have today and more about whether the adviser can provide sufficient value to justify their fees.

If you are unsure whether a particular adviser is likely to be suitable, it can be helpful to ask:

• Do you have minimum asset requirements?

• Do you charge fixed fees or percentage-based fees?

• What type of clients do you typically work with?

• How do you believe you could add value in my circumstances?

• What would a typical client journey look like?

Most advisers will be happy to discuss these points during an initial conversation.

It can also be beneficial to speak with more than one adviser before making a decision. Different firms can have very different philosophies, investment approaches, service models and charging structures. Taking time to compare options can help ensure you find an adviser whose approach aligns with your own preferences and objectives.

Ultimately, the most suitable adviser is not necessarily the largest firm, the cheapest firm or the firm with the most impressive marketing. It is the adviser who understands your objectives, communicates clearly, explains complex issues in a way you can understand and provides a service that you believe offers value for the fees being charged.

10.Managing Finances Yourself

Throughout this article, we have explored the potential benefits of financial guidance and regulated financial advice. However, it is important to recognise that many individuals successfully manage their own finances without ongoing professional support.

The growth of online platforms, educational resources, investment tools and financial information means that it is easier than ever to access information and implement financial decisions independently.

For some individuals, this approach may offer:

• Greater control over financial decisions

• Lower ongoing costs

• Flexibility in selecting products and investments

• The ability to make decisions at their own pace

• Increased understanding and engagement with personal finances

Many investors successfully manage their own investments by researching asset classes, understanding diversification principles and selecting investments through direct-to-consumer platforms.

There are also a range of ready-made and multi-asset investment solutions available for those seeking a simpler investment approach.

However, managing finances independently also carries responsibility.

Individuals must be comfortable researching options, understanding risks, monitoring investments, keeping up to date with legislative changes and making decisions without the benefit of professional recommendations.

Questions worth considering may include:

• Am I comfortable making financial decisions independently?

• Do I understand the risks involved?

• Do I have sufficient time to undertake research and reviews?

• Am I likely to remain disciplined during periods of market uncertainty?

• Am I confident that I understand the tax implications of my decisions?

• Do I know where to seek additional support if circumstances become more complex?

It is also important to recognise that managing finances yourself does not need to be an all-or-nothing decision.

Some individuals choose to manage everything independently. Others may seek financial guidance to better understand their options whilst retaining control of decision-making. Others may use regulated advice for specific areas whilst managing other aspects of their finances themselves.

The most appropriate approach will depend on your confidence, knowledge, objectives and the complexity of your circumstances.

Ultimately, there is no universally correct answer. The best approach is the one that provides you with sufficient understanding, confidence and support to make informed decisions whilst remaining comfortable with the level of responsibility you choose to retain.

11.Summary: Which Approach is Right for You?

One of the key themes throughout this article is that there is no single "correct" approach to managing your finances.

For some individuals, managing finances independently may provide sufficient flexibility, control and confidence. For others, financial guidance may help improve understanding, explore options and provide clarity regarding future plans. Some may ultimately decide that regulated financial advice is appropriate where personal recommendations, implementation support or additional consumer protections are required.

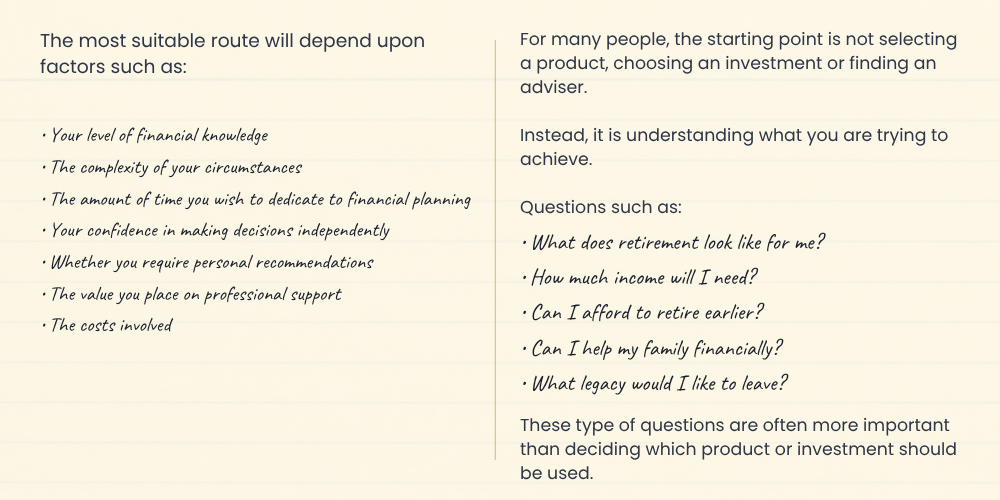

For many people, the starting point is not selecting a product, investment or adviser. It is understanding what they are trying to achieve and whether their current resources are likely to support those objectives. Once this is clear, it becomes much easier to determine whether managing finances independently, seeking financial guidance or obtaining regulated financial advice is the most appropriate next step.

At Clear Thinking Finance UK, the focus is on helping individuals gain greater clarity regarding their future financial plans through financial guidance, cashflow modelling and scenario testing. By improving understanding and exploring different outcomes, individuals can make more informed decisions and, where appropriate, engage with regulated financial advice with a clearer understanding of their objectives and requirements.

Whatever route you choose, taking the time to understand your options and make informed decisions is likely to be one of the most valuable investments you can make in your future financial wellbeing.

Further Reading

Need Help Understanding Your Options?

If you would like to better understand your retirement affordability, explore different scenarios or assess how your finances may support your future plans, Clear Thinking Finance UK provides financial guidance and cashflow modelling services designed to help bring greater clarity to your decision-making.

Using the same cashflow modelling tools used by many financial advisers, we can help you explore different outcomes, stress test assumptions and gain a clearer understanding of how your pensions, savings, investments and future plans may interact over time.

No product recommendations. No investment management. Just clear analysis, practical modelling and plain-English explanations to help you make more informed decisions.