What Is Financial Guidance and How Does It Work?

Introduction

When considering important financial decisions, many people assume there are only two options available: manage everything themselves or seek regulated financial advice.

In reality, there is often a middle ground.

Financial guidance can help individuals improve their understanding, explore different options and assess the potential implications of future decisions without receiving personal recommendations.

For some people, this may provide all the support they require. For others, it may help clarify objectives and identify areas where regulated financial advice could later be beneficial.

Understanding how financial guidance works can help determine whether it may be an appropriate option for your circumstances.

Key Takeaways

Financial guidance helps improve understanding and explore options.

Financial guidance does not provide personal recommendations.

Cashflow modelling can help illustrate the potential impact of different decisions.

Guidance can help identify risks, opportunities and areas requiring further consideration.

Responsibility for decisions remains with the individual.

Contents

1. What Is Financial Guidance?

Financial guidance focuses on helping individuals understand their financial position, identify potential options and explore the possible consequences of different decisions.

Rather than recommending a particular course of action, the objective is to provide information, analysis and clarity so that individuals can make more informed decisions themselves.

Guidance can be particularly valuable when considering major life events such as retirement, inheritance planning, pension decisions, changes in expenditure or significant financial commitments.

The emphasis is often placed on understanding objectives before considering potential solutions.

Many people spend considerable time researching products, investments or pension options before first establishing what they are trying to achieve. Financial guidance can help reverse this process by focusing initially on goals, priorities and future plans.

Financial guidance can help reverse this process by focusing initially on goals, priorities and future plans. Once the destination is clearer, it becomes easier to understand which options may be worth exploring further and where regulated advice may be required.

2. Financial Guidance vs Regulated Financial Advice

Although the terms are sometimes used interchangeably, financial guidance and regulated financial advice are very different services.

Financial guidance may help:

• Improve understanding

• Explain available options

• Explore different scenarios

• Model potential outcomes

• Highlight advantages and disadvantages

• Identify areas requiring further consideration

Regulated financial advice can additionally:

• Recommend specific products

• Recommend specific investments

• Recommend transfers or switches

• Arrange implementation

• Accept responsibility for recommendations

One way of thinking about the distinction is that guidance helps answer:

"What could happen if I did this?"

Whereas advice answers:

"What do you recommend I should do?"

Neither route is inherently better. The most suitable approach will depend on the complexity of the circumstances, the level of support required and the individual's confidence in making decisions.

3. Financial Guidance vs Managing Finances Yourself

Many individuals successfully manage their own finances without professional support.

The availability of online platforms, calculators, educational resources and financial information has made it easier than ever to take a do-it-yourself approach.

However, one challenge with managing finances independently is that it can sometimes be difficult to step back and objectively assess different options.

Financial guidance can provide an opportunity to discuss ideas, challenge assumptions and explore alternative scenarios without entering into a formal advisory relationship.

In many cases, the greatest value comes not from providing answers, but from helping individuals ask better questions.

4. Common Areas Where Financial Guidance Can Help

Financial guidance can be useful across a wide range of financial planning areas.

Common examples include:

• Retirement affordability

• Retirement timing decisions

• Pension options

• Income sustainability

• Pension contribution strategies

• Inheritance planning awareness

• Care funding considerations

• Helping family members financially

• Asset utilisation strategies

• Major expenditure decisions

The purpose is not to determine a single correct answer, but to improve understanding and assess how different decisions may affect future outcomes.

5. What Financial Guidance Cannot Do

Understanding what guidance cannot do is just as important as understanding what it can do.

Financial guidance cannot:

• Recommend specific investments

• Recommend pension transfers

• Recommend products or providers

• Manage investments

• Arrange implementation

• Provide regulated financial advice

Where regulated advice is required, guidance can help identify this and assist individuals in understanding what type of advice may be needed.

6. What Is Cashflow Modelling?

Cashflow modelling is one of the most powerful tools available within financial planning.

It brings together information such as:

• Income

• Expenditure

• Pensions

• Investments

• Savings

• Property assets

• Future objectives

The information is then used to create a projection illustrating how resources may support future plans over time.

Many financial advisers use cashflow modelling as part of the advice process. However, it can also be used independently within a guidance-based framework to help individuals better understand potential outcomes.

The purpose is not to predict the future with certainty.

Instead, it provides a structured framework for exploring possibilities and understanding how different decisions may affect future financial security.

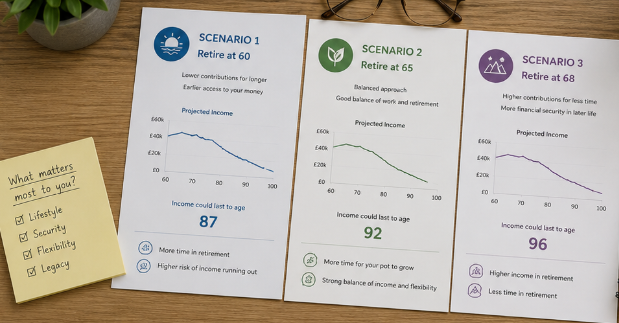

7. Exploring Different Scenarios

One of the greatest strengths of financial guidance is the ability to test different scenarios before making decisions.

Examples may include:

• Retiring earlier or later

• Increasing or reducing expenditure

• Taking tax-free cash

• Increasing pension contributions

• Helping children financially

• Drawing from different assets

• Downsizing property

• Adjusting investment assumptions

The ability to compare different scenarios side-by-side can often help individuals identify trade-offs and make more informed decisions.

8. Stress Testing Financial Plans

Financial plans rarely unfold exactly as expected. Stress testing helps assess how resilient a financial plan may be under less favourable conditions or unexpected costs arising.

This can include testing the impact of lower investment returns, higher inflation, increased spending, earlier retirement, care costs or living longer than expected.

Identifying potential vulnerabilities does not necessarily mean plans need to change. However, it can help individuals understand where risks exist and what actions may improve resilience.

9. What to Expect from Financial Guidance

Whilst the process will vary between providers, financial guidance will often involve:

• Understanding objectives

• Gathering relevant information

• Discussing priorities

• Cashflow modelling

• Scenario testing

• Exploring options

• Identifying risks and opportunities

• Providing educational support

Unlike regulated advice, the focus is not on providing recommendations but on improving understanding and helping individuals assess available options.

10. What to Expect from Clear Thinking Finance UK

As outlined above, the service provided by Clear Thinking Finance UK follows a guidance-based approach focused on improving understanding, exploring options and modelling potential outcomes without providing personal recommendations.

The process is designed to help individuals gain greater clarity regarding their financial position and the potential implications of different decisions before deciding on their next steps.

Initial Discussion

The process begins with an introductory discussion to understand the areas where support is required and the objectives you are hoping to achieve.

This may include topics such as retirement timing, retirement affordability, inheritance planning, pension decisions, care funding considerations or broader financial planning questions.

Information Gathering

Relevant information is collected to help build an accurate picture of your current position.

Depending on the work involved, this may include details of pensions, savings, investments, expenditure, assets and liabilities.

Cashflow Modelling and Scenario Analysis

Information is then incorporated into cashflow modelling software, allowing different scenarios to be explored and compared.

This may include testing alternative retirement dates, expenditure levels, pension strategies, inheritance objectives and other planning considerations.

Discussion and Review

A meeting is then used to review the outputs, discuss different scenarios and explore the potential implications of various options.

Questions can be raised, assumptions challenged and alternative scenarios tested in real time.

Summary Report

A written report is provided summarising the key discussions, assumptions and scenarios explored.

The report may also highlight areas requiring further consideration and identify where regulated financial advice may be beneficial.

No product recommendations are provided and no investments are managed.

The objective is simply to provide clear analysis, practical modelling and plain-English explanations to support better-informed decision making.

11. Is Financial Guidance Right For You?

Financial guidance may be suitable if you:

• Want greater clarity before making decisions

• Prefer to remain responsible for implementation

• Want to explore different scenarios

• Are unsure whether regulated advice is required

• Would benefit from cashflow modelling and financial planning support

• Want to better understand the potential implications of future decisions

12. Summary

Financial guidance occupies a middle ground between managing finances entirely yourself and obtaining regulated financial advice.

For many people, understanding their objectives and exploring different scenarios is the most valuable first step.

By helping individuals understand their options, assess potential outcomes and stress test future plans, financial guidance can provide greater clarity and confidence when making important financial decisions.

Further Reading

Need Help Understanding Your Options?

If you would like to better understand your retirement affordability, explore different scenarios or assess how your finances may support your future plans, Clear Thinking Finance UK provides financial guidance and cashflow modelling services designed to help bring greater clarity to your decision-making.

Using the same cashflow modelling tools used by many financial advisers, we can help you explore different outcomes, stress test assumptions and gain a clearer understanding of how your pensions, savings, investments and future plans may interact over time.

No product recommendations. No investment management. Just clear analysis, practical modelling and plain-English explanations to help you make more informed decisions.