What Happens When You Work With a Financial Adviser?

Introduction

Many people understand what a financial adviser does in broad terms, but far fewer understand what actually happens once they decide to seek advice.

The financial advice process is often much more structured than people expect. Before making recommendations, advisers are required to gather information, understand objectives, assess risk and document why any proposed course of action is suitable.

Understanding how this process works can help you decide whether regulated financial advice is appropriate for your circumstances and what level of service you may wish to receive.

Key Takeaways

Financial advice involves much more than selecting investments.

Advisers must follow a structured suitability process.

Recommendations are based on your objectives, circumstances and risk profile.

Many advisers use model portfolios or discretionary fund managers.

Understanding how advisers operate can help you assess whether fees represent good value.

Contents

1.The Typical Financial Advice Process

The purpose of financial advice is not simply to recommend products.

At its core, financial advice is designed to help individuals make informed decisions and achieve their financial objectives.

Whilst every advisory firm will have its own processes and areas of specialism, there are a number of common stages that most clients can expect when engaging a financial adviser.

2.Common Questions About the Advice Process

Why advisers collect all of this information?

Before making recommendations, advisers need to understand your financial position, objectives, family circumstances, existing arrangements and attitude to risk. This information helps ensure recommendations are appropriate for your circumstances and objectives.

Some questions may be more personal than expected, such as your health or even your weight. Most advisory firms use a structured questionnaire, often referred to as a factfind, to gather information consistently across all clients. While some questions may appear unrelated to the advice being sought, they often help identify suitable solutions or rule out others. For example, your health could influence how long income may be required, appropriate investment timeframes, the financial impact on a spouse or partner, eligibility for enhanced annuity rates, suitability for protection policies and more.

Why Do I Need To Sign A Client Agreement?

Client agreements explain the services being provided, how advisers are paid, the responsibilities of each party and any important terms that apply to the relationship.

These documents are designed to ensure both parties understand what services are being provided and what can be expected moving forward. This is also a regulatory requirement before advice can be given.

Why Do I Need To Provide ID?

Advisers are also required to verify the identity of their clients as part of anti-money laundering regulations. This will typically involve photographic identification and proof of address, although requirements can vary between firms.

Why Are Suitability Reports Required?

Every recommendation the adviser makes is known as an advice point. This applies equally to recommending a change and recommending no change at all.

The report will usually explain the reasons for the recommendations, the potential disadvantages and risks, and any charges that may apply from the advisory firm, product provider and underlying investments.

For a relatively simple advice point, such as making a withdrawal when you only have one arrangement to do this from, you may also receive this via email with a short justification and covering the relevant areas.

Why recommendations can take time?

Many people are surprised by the amount of work that takes place behind the scenes.

Depending on the circumstances, advisers may need to:

Obtain information from pension providers (often one of the biggest sources of delay)

Analyse existing arrangements

Carry out product and investment research

Prepare cashflow modelling

Consider tax implications

Document suitability

The time required will vary depending on the complexity of the case and the information available.

Why Can't Advisers Simply Tell Me What To Do?

Regulated financial advice requires advisers to understand your circumstances before making recommendations.

A recommendation that may be suitable for one person could be entirely inappropriate for another. As a result, advisers are required to gather information, assess suitability and explain why recommendations are considered appropriate.

3.Ongoing Reviews

Many advisory firms offer an ongoing service.

The purpose of ongoing reviews is to ensure arrangements remain aligned with objectives as circumstances evolve.

Reviews may include:

Investment performance reviews

Cashflow updates

Retirement planning reviews

Tax planning discussions

Estate planning considerations

Legislative updates

Changes to personal circumstances

The frequency and scope of reviews can vary significantly between firms.

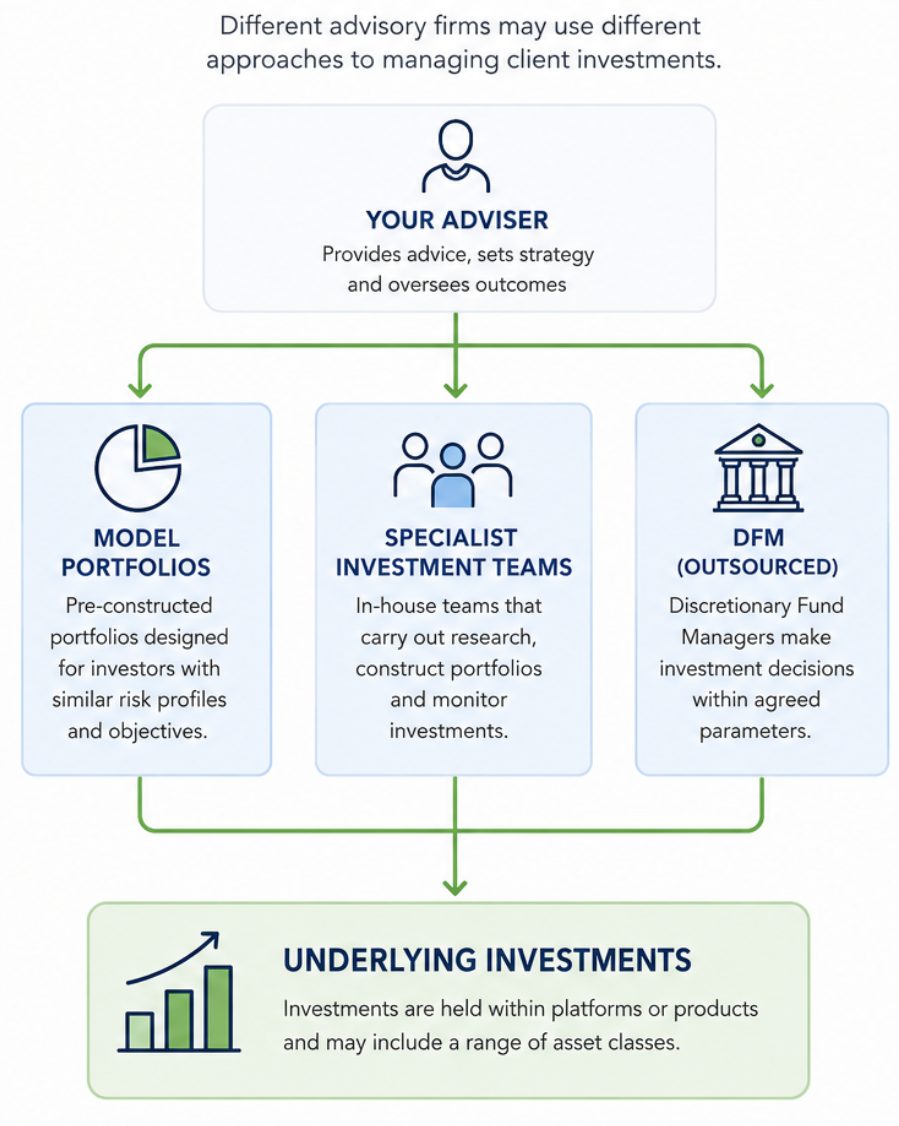

4.Different Ways Investments May Be Managed

The approach adopted will depend on the firm's structure, resources and philosophy. Understanding how investments are managed can help you better assess the overall service being provided and the charges being incurred.

5.Model Portfolios

Many advisory firms use model portfolios rather than selecting investments individually for each client.

A model portfolio is a pre-constructed investment strategy designed for a particular level of risk, such as cautious, balanced or adventurous. Once selected, clients with similar objectives and risk profiles are invested into the same underlying portfolio.

This approach can provide consistency, simplify administration and allow portfolios to be monitored and updated efficiently across a large number of clients.

Potential advantages may include:

• Consistent investment management

• Ongoing monitoring and governance

• Access to investment committees and research

• Simplified administration

• Easier implementation of portfolio changes

• Greater consistency of client outcomes

Model portfolios may be managed directly by an advisory firm's investment team, outsourced to a third party, or constructed using recommendations from investment research providers.

Where advisory firms operate their own model portfolio propositions, the Adviser Fund Index (AFI) can provide a useful comparison point. AFI publishes data across a range of risk categories, including cautious, balanced and aggressive portfolios, helping investors understand how adviser model portfolios compare against similar solutions in the wider market.

Where discretionary fund managers are being used, Asset Risk Consultants (ARC) benchmarks are more commonly used to compare discretionary managers operating within similar risk categories. Should the DFM not be registered with ARC then the AFI can still be a useful comparator.

It is important to understand that these benchmarks primarily focus on investment performance and investment management costs. They do not typically include the wider services that may be provided through an advisory relationship, such as financial planning, retirement modelling, tax planning, regular reviews and ongoing client support.

Investment performance should always be considered, as it forms an important part of achieving long-term financial objectives. The returns achieved, the level of risk taken and the costs incurred can all have a significant impact on outcomes over time.

When reviewing investment performance, it is also important to understand the benchmark being used for comparison.

Advisers, DFMs and investment managers may use different benchmarks depending on the objectives, risk profile and composition of a portfolio. While these benchmarks can provide useful context, they may not always reflect the comparison that is most relevant to your circumstances.

If you are unsure whether a benchmark is appropriate, consider asking why it has been selected, whether alternative comparisons are available (such as ARC or AFI for performance compares against broader peer groups). Many firms will be able to provide additional comparisons on request.

The objective is not simply to determine whether a portfolio has outperformed a benchmark, but whether it has delivered an appropriate outcome relative to the level of risk taken, the costs incurred and the objectives it was intended to achieve.

6.Discretionary Fund Managers (DFMs)

As investment portfolios grow in size and complexity, some investors and advisory firms choose to use a Discretionary Fund Manager (DFM).

A DFM is responsible for making investment decisions on behalf of investors within agreed risk parameters and objectives. Rather than requiring approval for every investment change, the DFM is given authority to manage portfolios on an ongoing basis.

This can provide access to specialist investment expertise and allow portfolio changes to be implemented more quickly when market conditions or investment opportunities change.

Many advisory firms utilise DFMs as part of their investment proposition, allowing advisers to focus on wider financial planning matters while investment management is delegated to specialists.

Potential advantages of using a DFM may include:

• Access to dedicated investment professionals

• Ongoing portfolio monitoring and governance

• Faster implementation of investment changes

• Access to specialist investment research and resources

• The ability for advisers to focus on wider planning considerations

However, there are also considerations that investors may wish to explore. Where a DFM is being recommended, it can be helpful to understand:

• Why the DFM has been selected

• Whether alternative solutions were considered

• How performance is monitored

• The charges being incurred

• How the DFM compares against appropriate peer groups

Many DFMs are assessed against Asset Risk Consultants (ARC) benchmarks, which compare discretionary managers operating within similar risk categories. While past performance should never be the sole basis for decision-making, such comparisons can provide useful context when assessing a discretionary investment proposition.

It is also worth recognising that advisory firms operate in different ways. Some firms have close relationships with one or more DFMs, while others may offer access to a wider range of discretionary managers. In larger firms, acquisitions and business consolidation have increasingly led to centralised investment propositions designed to create consistency across the business with an in-house DFM.

This does not necessarily mean one approach is better than another. Some investors may value the governance and consistency of a centralised proposition, while others may prefer a more bespoke approach or greater involvement in investment decisions.

As with any investment solution, the objective should not simply be to select a DFM, but to determine whether the overall proposition is suitable for your circumstances, objectives and preferences.

7.Discretionary vs Advisory Investment Management

When reviewing investment propositions, it can be useful to understand the difference between discretionary and advisory management.

While the terms are often used within the industry, many investors are unaware of the distinction or the practical implications for how investment decisions are made.

Advisory Management

Under an advisory arrangement, recommendations are made to the client, but the final decision remains with the client.

For example, an adviser may recommend changes to investments, asset allocation or portfolio structure, but approval is normally required before those changes are implemented.

Potential advantages include:• Greater involvement in investment decisions

• More control over portfolio changes

• The opportunity to challenge or discuss recommendations before implementation

However, obtaining approval for changes can take time and may result in delays where market conditions are changing quickly.

Discretionary Management

Under a discretionary arrangement, authority is delegated to an investment manager or DFM to make investment decisions within agreed parameters and risk limits.

This allows portfolio changes to be implemented without seeking approval for every adjustment.

Potential advantages include:

• Faster implementation of investment decisions

• Ongoing professional portfolio management

• Reduced administration

• The ability to respond more quickly to market developments

However, investors are placing greater reliance on the investment manager's expertise and governance processes.

Which Approach Is Better?

Neither approach is inherently better.

Some investors prefer maintaining a high level of involvement and control over investment decisions, while others value the convenience and responsiveness that discretionary management can provide.

It is also worth remembering that discretionary and advisory services can exist alongside wider financial planning support. An adviser may provide financial planning and recommendations while using a discretionary manager for investment management, or they may provide both planning and investment oversight directly.

Understanding who is responsible for decisions, how those decisions are made and what level of involvement you wish to retain can help determine which approach is most appropriate for your circumstances.

8.Product Selection and Adviser Propositions

Product selection is an area where regulated advice may add significant value, particularly where multiple options appear suitable or where tax considerations are involved.

Many people assume recommendations will be selected individually from the entire market and tailored completely from scratch. Whilst this may sometimes be the case, it is important to understand that many advisory firms operate structured investment and platform propositions designed to provide consistency across their client base.

These propositions may include:

• Preferred investment platforms

• Approved product panels

• Model portfolios

• Discretionary Fund Managers (DFMs)

• Centralised investment propositions

• In-house investment solutions

When assessing potential solutions, advisers will often consider both the product itself and the provider offering it. Factors may include:

• Charges

• Available investment options

• Drawdown functionality

• Death benefit considerations

• Online functionality

• Administration standards

• Adviser servicing capabilities

• Long-term suitability

The rationale behind structured propositions is often to improve efficiency, governance, oversight and consistency. By concentrating research and monitoring on a smaller range of solutions, firms can often provide a more robust and scalable service to clients.

However, this can also mean that the range of solutions considered may be narrower than some clients expect.

In recent years, acquisitions and consolidation within the financial advice profession have become increasingly common. As firms grow, it is often necessary to introduce greater standardisation to ensure advice processes remain consistent across a larger client base.

As a result, it is not unusual for clients to be recommended a particular platform, investment proposition or DFM that forms part of the firm's preferred approach.

Where an adviser recommends moving assets, it can be helpful to understand:

• Why the existing arrangement may not be suitable for ongoing servicing

• Whether the recommended platform forms part of the firm's preferred proposition

• What alternatives were considered

• The impact on charges

• The benefits and drawbacks of transferring

• Whether future flexibility may be affected

Some providers also offer adviser-specific versions of products or can be adapted to fit an adviser's servicing proposition, making them easier for firms to administer and support on an ongoing basis.

It is also worth remembering that two products that appear very similar on the surface may offer significantly different features and capabilities over the long term. This can become particularly important during retirement, where income withdrawal flexibility, beneficiary planning, estate planning considerations and ongoing servicing requirements may play a larger role.

This does not mean recommendations made through structured adviser propositions are unsuitable. In many cases there may be genuine benefits in terms of administration, governance, reporting, investment oversight and overall client experience. However, understanding the reasons behind a recommendation can help ensure expectations remain aligned.

Smaller advisory firms may sometimes offer a broader range of platform and investment options or provide greater flexibility in accommodating individual preferences. Larger firms may more commonly utilise centralised propositions, approved panels or in-house investment solutions. Neither approach is inherently better, but understanding how a firm operates can be useful when selecting an adviser whose approach aligns with your own preferences and objectives.

Where discretionary investment management is involved, it can also be useful to understand how performance is monitored, what benchmarks are used and whether comparisons are made against peer groups such as the ARC Wealth Indices.

9.Understanding Charges

Charges are often one of the most discussed aspects of financial planning and investment management. Whilst costs are important, they should generally be considered alongside the value being provided and the objectives being achieved.

Depending on the route chosen, there may be several layers of charges to consider.

Financial advisers typically charge either a percentage of assets under management, a fixed fee, or a combination of the two.

Percentage-based ongoing adviser charges commonly range from around 0.5% to 1.0% per annum (plus VAT where applicable), although this can vary significantly depending on the level of service being provided and the complexity of the client's circumstances.

Some clients question why they may pay the same percentage-based adviser charge as another client with significantly lower levels of wealth.

Advisory firms will often argue that the complexity of circumstances, professional responsibility, regulatory obligations, ongoing monitoring requirements and potential liability associated with providing advice do not necessarily increase or decrease in direct proportion to the size of a portfolio. In addition, larger portfolios may involve more complex tax planning, estate planning and retirement income considerations.

However, it is also reasonable for clients to consider whether the charges being incurred remain proportionate to the level of service and value being received. If you feel this may not be the case, it is entirely appropriate to discuss this with your adviser. Some firms offer tiered charging structures, discounted rates for larger portfolios or bespoke fee arrangements where circumstances warrant this.

Some advisers may instead offer fixed-fee arrangements, although these can be less common and may not always be suitable for every client.

It is important to understand that adviser charges are often only one component of the overall cost. Depending on the solution being recommended, there may also be platform charges, investment fund charges and, where applicable, discretionary investment management charges.

As a result, the total cost of ownership can sometimes be higher than initially expected if all layers of charges are not considered together.

When assessing charges, useful questions may include:

• What services am I receiving?

• How often will reviews take place?

• What support is available between reviews?

• What ongoing work is being carried out on my behalf?

• How are investments being monitored?

• Are there additional DFM or platform charges?

• What is the total annual cost once all charges are combined?

Ultimately, charges should not be viewed in isolation. A lower-cost solution that fails to meet your objectives may be poor value, whilst a higher-cost solution that delivers meaningful planning, support and confidence may represent excellent value.

The key consideration is whether the service, expertise and support being provided justify the costs being incurred.

10.Question to Ask Before Appointing An Adviser

Before choosing an adviser, consider asking:

Are you Independent or Restricted?

Do you specialise in particular areas?

What services do you provide?

How are you paid?

Do you use model portfolios?

Do you use a DFM?

What ongoing service is provided?

How often are reviews conducted?

Do you have minimum asset requirements?

How do you believe you could add value in my circumstances?

Comparing several advisers can often help identify the most suitable fit.

11.Summary

Financial advice is typically much more than selecting investments or recommending products.

A structured process exists to help ensure recommendations are appropriate, risks are understood and objectives remain at the centre of decision-making.

Understanding how advisers operate, how investments are managed and how charges are structured can help you make a more informed decision when considering whether regulated financial advice is right for you.

The most suitable adviser is not necessarily the cheapest or the largest. It is the adviser whose approach, services and communication style align most closely with your objectives and circumstances.

Need Help Understanding Your Options?

If you would like to better understand your retirement affordability, explore different scenarios or assess how your finances may support your future plans, Clear Thinking Finance UK provides financial guidance and cashflow modelling services designed to help bring greater clarity to your decision-making.

Using the same cashflow modelling tools used by many financial advisers, we can help you explore different outcomes, stress test assumptions and gain a clearer understanding of how your pensions, savings, investments and future plans may interact over time.

No product recommendations. No investment management. Just clear analysis, practical modelling and plain-English explanations to help you make more informed decisions.